Construction accounting tracks money by project, not just for the whole company. Each job has its own budget, crew, and timeline, so you need to know which ones make money and which ones bleed it. That is the core difference from standard bookkeeping, and it shapes how you cost jobs, recognize revenue, bill clients, and run payroll.

How is construction accounting different from regular accounting?

Standard accounting follows a steady stream of simple transactions. Construction does not. Most contractors run several jobs at once, each lasting weeks, months, or years, and each spread across different sites.

A few things set it apart:

- Project-based tracking. You watch costs and profit job by job, often for many jobs at the same time.

- Decentralized work. Crews work across many sites, so data has to come in from the field. A QuickBooks integration helps pull that data into one place.

- Long contracts. Jobs can run for years and depend on progress payments, not one lump sum at the end.

- Change orders. Scope shifts often, and each change affects cost and schedule, so it needs a clean paper trail.

If QuickBooks alone has felt like a poor fit, see why contractors struggle with QuickBooks.

What is job costing?

| Cost code | Budget | Actual to date | Variance | |

|---|---|---|---|---|

| Labor | $38,000 | $41,300 | -$3,300 | |

| Materials | $27,500 | $26,100 | +$1,400 | |

| Subcontractors | $18,000 | $18,000 | $0 | |

| Equipment & other | $6,500 | $7,050 | -$550 |

Job costing means tracking every cost tied to a specific job, so you can see profit per project instead of one company-wide number. You assign labor, materials, and sub costs to the job that created them.

Done right, job costing shows where you are overspending while there is still time to fix it. Our free job cost tracker template is a simple budget vs actual sheet to start with. Tools that pull your estimates into the same system make this easier, since budget and actuals sit side by side. For more, see our guide to real-time job costing.

What financial reports should contractors track?

A few reports tell you most of what you need to know:

- Profit and loss shows income against expenses over a period.

- Balance sheet shows what you own and owe at a point in time.

- Cash flow statement shows money in and out, which matters most when payments lag.

Real-time data from time-tracking makes these reports accurate instead of stale.

How does revenue recognition work in construction?

Revenue recognition is when you count income on the books. Three methods are common:

- Cash basis: Count revenue when payment lands. Simple, but it can hide the real health of long jobs.

- Completed contract: Count revenue only when the job is done. Clean, but lumpy.

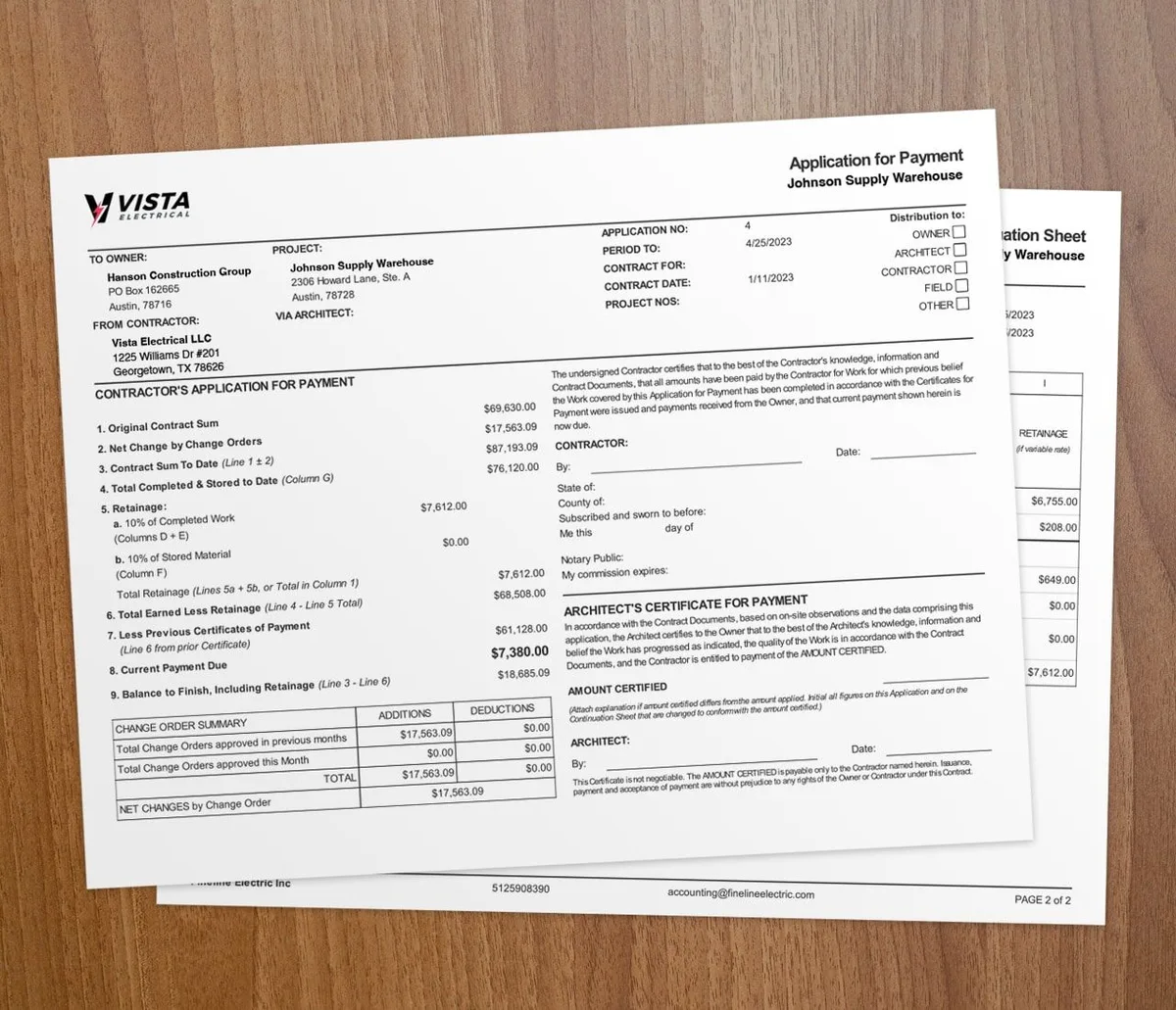

- Percentage of completion: Spread revenue across the life of the job. It lines up with AIA-style billing and percent-complete invoicing.

Retainage is the slice of each payment the owner holds back until the job is done or hits a milestone. It usually runs 5% to 10%, though it varies by contract and state. Track every held dollar so you collect it at the end.

What are the main construction billing methods?

| Line item | App 1 | App 2 | App 3 |

|---|---|---|---|

| Rough-in | 40% | 75% | 100% |

| Panels & gear | 0% | 30% | 60% |

| Fixtures | 0% | 0% | 25% |

The way you bill depends on the job:

- Time and materials: Charge for actual hours and materials used. Clients see a full cost breakdown. See the time and materials feature.

- Fixed price: Set one price for the whole job. Predictable, but risky if costs run over your estimate.

- Unit price: Charge per unit of work. Good for repeatable, countable tasks.

- AIA-style progress billing: Invoice by percent complete using G702 and G703 forms. Common on longer commercial contracts, and it keeps cash flowing.

How do you handle construction payroll?

Payroll in construction comes with extra rules:

- Certified payroll: Government-funded jobs require weekly reports confirming you paid the correct prevailing wage.

- Union payroll: Adds wage scales, benefits, and dues set by union agreements.

- Multi-state payroll: Crews across state lines mean different tax and labor rules per state.

- Compliance: Tax laws and reporting standards change, so you have to keep up.

Connecting payroll to your books with payment processing cuts manual entry and errors. For the obligations behind each paycheck, see our guide to contractor payroll liabilities.

When do you need construction accounting software?

You need it once you run more than one job at a time and have to know profit per project. If you bill in phases, track retainage, or manage change orders, purpose-built software like Werx saves real hours and protects your margin.

A solo operator doing a few small cash jobs can get by with simpler tools for now. But as soon as you carry crews, subs, and multiple open contracts, generic bookkeeping starts to cost you. To compare your options, read how to choose construction accounting software.

Key takeaways

- Construction accounting tracks profit by job, not just for the whole company.

- Job costing assigns labor, materials, and sub costs to the job that created them.

- Retainage usually runs 5% to 10% and is held until the job is done. Track every dollar.

- Billing methods include time and materials, fixed price, unit price, and AIA progress billing.

- Contractor software like Werx connects estimates, time, billing, and QuickBooks in one system.